What Is A “Safe” Portfolio Withdrawal Rate In Retirement?

- zach5896

- Jan 22, 2024

- 4 min read

Updated: Jul 27, 2024

Summary/TLDR

Getting your portfolio withdrawal rate “right” will make the difference between remaining retired and running out of money. The popular rule-of-thumb known as the 4% Rule was never intended to be used in practice and has a lot of shortcomings compared to my preferred approach, known as the Guardrails strategy. Finally, no portfolio withdrawal strategy is complete without an asset allocation strategy.

Introduction

Your portfolio withdrawal rate is the rate, expressed as a percentage, at which you are distributing funds from your portfolio. For example, if you are taking distributions of $50,000/yr from a $1,000,000 portfolio, then your portfolio withdrawal rate is 5% ($50,000 / $1,000,000).

Your withdrawal rate is a very important number to be mindful of during retirement because, if it is too high, you will risk drawing your portfolio down to $0. Your portfolio withdrawal rate should be high enough to make sure you are getting the most out of your nest egg, but low enough that it’s not outpacing the long-term growth of the internal investments as well.

A Few Examples

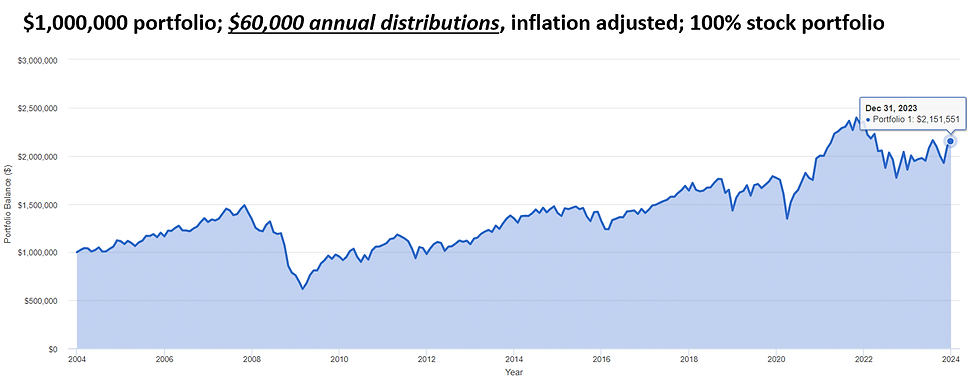

For example, someone who retired 20 years ago today with a $1,000,000 portfolio who withdrew 10% annually (adjusted for inflation) would have run out of money by 2016 after their portfolio was decimated during the 2008 financial crisis.

However, if this person had started by withdrawing only $50,000 from their portfolio (adjusted for inflation), they would have a portfolio worth over $2,000,000, despite going through the same crash in 2008.

Clearly, making sure that your portfolio withdrawal rate is sustainable is an imperative matter in your retirement plan. Mountains of research has been done on portfolio withdrawal rates which has culminated in a “rule of thumb” known by many as the 4% Rule.

The 4% Rule

Many have heard of the so-called “4% Rule”, which serves as the current paradigm for what a “safe” withdrawal rate is. The 4% Rule states that one can “safely” maintain a distribution amount equal to 4% of your portfolio value on the day you retire, adjusted annually for inflation. For example, assuming an inflation rate of 3%, if I retire with a portfolio value of $1,000,000, then I will withdraw $40,000 in year one. In year two, I will withdraw $41,200, regardless of my portfolio value. In year 3, I will withdraw $42,436, again regardless of my portfolio value. So on, and so forth.

What many don’t know about the 4% Rule, however, is that it was only an academic exercise and was never intended to be an actual retirement withdrawal strategy. Consequently, it comes up short in many aspects.

The 4% Rule will likely leave a lot on the table for retired clients who, as will be seen below, can usually afford to distribute much more than 4% without any fear of running out of money as long as a few simple rules are followed. Furthermore, the 4% Rule has no guidance for how to invest one’s portfolio between stocks and bonds (this is known as “asset allocation), which is a vitally important question in retirement planning.

The Guardrails Strategy

The distribution strategy I use in my practice, known as the “Guardrails” strategy, is based on research that was actually intended to be used in practice. The strategy works something like this (for the sake of this post, I’ve omitted specific numbers and percentages used in some of the “rules” listed below).

When one retires, they can begin withdrawing somewhere between 4% and 6% of their current portfolio value (the most commonly referred to starting point is 5.4%)

Every year, they can adjust their distribution for inflation

When their portfolio value falls beyond a certain amount (known as the “Lower Guardrail”), due to market fluctuations or excessive distributions, their distribution rate will be adjusted down

When their portfolio value rises beyond a certain amount (known as the “Upper Guardrail”), due to market fluctuations or additional contributions, their distribution rate can be adjusted up

Adjustments should be made for those who retire “early” or those who retire “late”

A visual representation of these rules would look like this:

The research behind this distribution model showed exceptionally high confidence levels for those who follow the rules correctly, all while allowing them to take far more in income from their portfolios than what is prescribed in the 4% Rule.

As mentioned above with the 4% Rule, no distribution strategy is complete without an asset allocation strategy. As with the 4% Rule, the Guardrails model will fail if asset allocation is not dialed in. The strategy that I employ in my practice with retired clients is quite simple:

1 years’ worth of distributions is invested in the money market (this is where monthly distributions are taken from).

4 years’ worth of distributions are invested in a short-term bond fund.

The rest of the portfolio is invested in a diversified mix of stock index funds.

If stocks have risen by the time the money market fund is depleted, then stocks are sold to purchase more money market funds. The entire portfolio is also rebalanced as needed.

If stocks have fallen by the time the money market fund is depleted, then bonds are sold to purchase more money market funds. No further rebalancing takes place.

Having a distribution plan like the Guardrails Strategy in place will grant you peace of mind during times of market volatility. And as long as you’re willing to “tighten your belt” when times get hard, you can confidently take more from your portfolio and increase your standard of living.